DSV acquire DB Schenker creating logistics market leader

Written by Quorica Capital M&A team – Adam Tahri

Introduction:

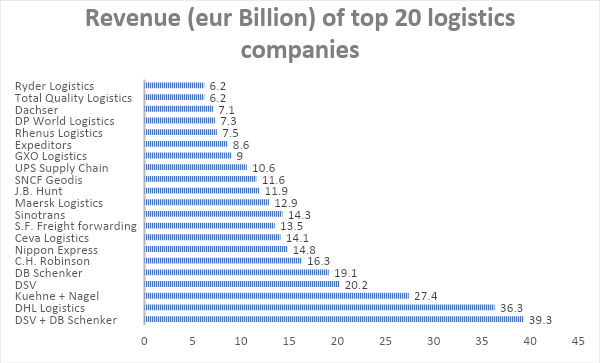

In September 2024 DSV announced its acquisition of Schenker for 14.3 billion euros. This deal represents a pivotal move in the logistics sector, cementing DSV’s position as a global logistics leader. The merger is expected to significantly reshape the competitive landscape in logistics by enhancing operational efficiency and market presence, in Europe, North America and APAC. DB Schenker was a Deutsche Bahn subsidiary, the sale of a non-core business allows a significant reduction in debt and the ability to focus on its core railway business in Germany. The subsidiary was put up for sale last year and drew interest from other potential suitors including CVC, however it was DSV who emerged with the best proposition as DB Schenker was the most valuable to them due to the synergies we will discuss below.

Deal overview:

- Acquirer: DSV

- Target: DB Schenker

- Price: 14.3 billion euros

- EV/EBIT: 14x (2024 Industry average 11.2x)

- EV/Revenue: of 0.77x (2024 Industry average 0.9x)

- Deal Structure: All-Cash Transaction financed through a combination of equity raise (4-5 billion euros) and debt

- Announcement Date: September 2024

- Expected Closing Date: Q2 2025

- Buy-Side Advisors: Goldman Sachs, Deutsche Bank

- Sell-Side Advisors: Rothschild & Co

Market Consolidation:

The logistics market is highly fragmented with the top 20 players only representing 30-40% of market share and due to this fragmentation, it is hard to be efficient. This acquisition will see the combined entity take 6-7% of the logistics market share and become the leading logistics provider (based on pro-forma revenue). The merged company will operate in over 90 countries with a workforce of 147,000 employees.

Operational and supply chain Synergies:

With both companies having extensive road, sea and air freight networks, the integration will likely result in cost savings due to economies of scale. The acquisition should also provide additional cross-selling opportunities, as well as stronger network and service offerings. DSV’s 10.5% EBIT margin significantly outperforms DB Schenker’s 5.5%, a key focus area in terms of operational improvements. One of the main goals for DSV will be to elevate Schenker’s margins to match its own, primarily by driving operational efficiencies. The integration process, like DSV’s previous acquisitions of Panalpina and Agility, is expected to yield around €2.2 billion in synergies. DSV’s strategy for margin improvement involves moving Schenker’s operations onto DSV’s IT architecture and streamlining headcount, a tactic that has successfully lifted margins in prior deals. DSV’s management has expressed optimism about raising Schenker’s operating margins within three years, although achieving DSV’s higher EBIT margin will be challenging due to Schenker’s larger operational scale compared to previous acquisitions.

Risks and Execution Challenges:

While the acquisition is expected to boost DSV’s financial performance significantly, there are execution risks, particularly related to Schenker’s workforce. DSV has committed to maintaining employment levels in Germany for at least two years post-acquisition, which may delay the full realisation of cost savings. Additionally, DSV’s history of volume churn in its air, sea, and road businesses during past integrations signals the potential for near-term disruptions, with anticipated churn rates between 15-25%.

This churn is driven by several factors:

- Operational Disruptions: Integrating freight systems across road, sea, and air often leads to temporary delays or inefficiencies, prompting customers to seek alternatives.

- Customer Uncertainty: Concerns over pricing and service continuity may cause Schenker’s clients to switch to competitors.

- Employee Retention: Workforce challenges, particularly with key personnel, could affect service quality, further increasing churn.

The financial impact could be significant. With DB Schenker’s 2023 revenue at approximately €20 billion, a 15-25% churn could result in a €3-5 billion revenue loss, primarily in air and sea freight. Additionally, Schenker’s lower EBIT margin (5.5% vs. DSV’s 10.5%) means the deal could pressure DSV’s profitability in the short term. Disruptions to working capital cycles and thus cash flow are also likely, as fewer shipments could delay receivables.

However, DSV’s track record of integrating large acquisitions suggests that while short-term pain is expected, the long-term benefits from synergies, economies of scale, and expanded market reach should outweigh initial losses. DSV has historically restored lost volumes within 2-3 years and expects similar results with Schenker.

Industry effects:

DSV and Schenker both have significant operations in Europe and North America, two critical logistics regions. In Europe, the deal is expected to enhance DSV’s reach within key transportation and logistics corridors, allowing the company to provide even more efficient and cost-effective services. Additionally, DSV plans to invest €1 billion in Germany over the next 3-5 years, cementing Germany as a critical market for its growth. This could create ripple effects across Europe, where DSV may attract a greater share of cross-border logistics, thus intensifying competition with DHL and other European logistics providers. The acquisition could also spur further consolidation in the industry as other companies seek to scale up to compete with DSV’s enhanced capabilities

Conclusion:

In summary, DSV’s acquisition of DB Schenker represents a strategic move to bolster its market share and operational capabilities, especially in Europe and North America. While there are short-term integration challenges and risks, the long-term benefits of enhanced service offerings, operational synergies, and improved financial performance should solidify DSV’s leadership in the global logistics industry.

Written by Quorica Capital M&A team – Adam Tahri